signalmankenneth

Verified User

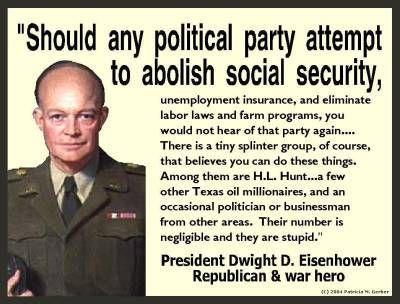

Even for Congress. They, and others who apparently don't study the facts, believe that Social Security is a government handout. But 'entitlement' means that people who have paid into a program all their lives are entitled to a reasonable return on their investment. A better definition, as pointed out by Mark Karlin at Truthout, is a "mandated retirement savings plan."

Cutting this popular and well-run and life-sustaining program would be irrational. There are many reasons for this.

1. Americans Have Paid For It Throughout Their Working Lives

As of 2010, according to the Urban Institute, the average two-earner couple making average wages throughout their lifetimes receive less in Social Security benefits than they paid in. Same for single males. Same by now for single females. One-earner couples get back more than they paid in.

2. It's a Small Benefit, But Most Seniors Depend On It

The average Social Security benefit is less than $15,000 a year, but most of our seniors rely on this for the majority of their income. Even the second richest quartile of Americans depends on Social Security for over half of its retirement income.

3. It's Been Well-Run for Over Half a Century

The poverty rate has decreased dramatically over the past 50 years, in large part because of the benefits of the Social Security program.

Social Security is running on a surplus of $2.6 trillion, it's funded until 2037, it cannot run out of money, it cannot contribute to the deficit, it has lower administrative costs than private sector 401k retirement plans, and it's wildly popular.

On top of all this, a report by the AARP Public Policy Institute found that Social Security stimulates the economy, adding more than $1 trillion to the U.S. economy each year as recipients spend their benefits on goods and services.

Dean Baker calls Social Security "perhaps the greatest success story of any program in US history."

4. The Free-Market Alternative Doesn't Work

The free-market alternative is everybody for themselves. That's fine for people with good jobs and retirement plans. But stunningly, the number of private sector workers covered by a pension with a guaranteed payout has dropped from 60 percent to 10 percent in a little over thirty years.

Americans are going into debt faster than they're saving for retirement, and those able to put something aside often make wrong choices with their money.

Financial experts, who generally speak for the people with enough money to hire a financial expert, tell us to have $200,000 to $300,000 in personal retirement savings. Most Americans have about a tenth of that, less than $25,000.

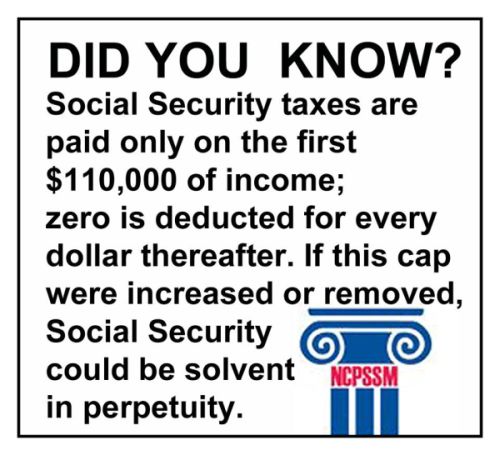

5. Redistribution Has Moved Retirement Money from the Middle Class to the Rich

Tax Expenditures -- subsidies from special deductions, exemptions, exclusions, credits, capital gains, and loopholes that move tax money to the richest taxpayers -- are estimated to be worth up to 8% of the GDP, or about $1.2 trillion.

That alone is more than enough to pay for Social Security ($883 billion).

Because of this misdirected revenue, government has been forced to borrow from Social Security to fund its programs. Most notably, George W. Bush took our retirement money to pay for his two wars and his tax cuts for the rich.

This last reason, more than any of the others, reveals the overwhelming unfairness of cutting Social Security. In effect, the middle class is being told to replenish its own savings account after those savings were passed along to the military and the super-rich.

By PAUL BUCHHEIT

Cutting this popular and well-run and life-sustaining program would be irrational. There are many reasons for this.

1. Americans Have Paid For It Throughout Their Working Lives

As of 2010, according to the Urban Institute, the average two-earner couple making average wages throughout their lifetimes receive less in Social Security benefits than they paid in. Same for single males. Same by now for single females. One-earner couples get back more than they paid in.

2. It's a Small Benefit, But Most Seniors Depend On It

The average Social Security benefit is less than $15,000 a year, but most of our seniors rely on this for the majority of their income. Even the second richest quartile of Americans depends on Social Security for over half of its retirement income.

3. It's Been Well-Run for Over Half a Century

The poverty rate has decreased dramatically over the past 50 years, in large part because of the benefits of the Social Security program.

Social Security is running on a surplus of $2.6 trillion, it's funded until 2037, it cannot run out of money, it cannot contribute to the deficit, it has lower administrative costs than private sector 401k retirement plans, and it's wildly popular.

On top of all this, a report by the AARP Public Policy Institute found that Social Security stimulates the economy, adding more than $1 trillion to the U.S. economy each year as recipients spend their benefits on goods and services.

Dean Baker calls Social Security "perhaps the greatest success story of any program in US history."

4. The Free-Market Alternative Doesn't Work

The free-market alternative is everybody for themselves. That's fine for people with good jobs and retirement plans. But stunningly, the number of private sector workers covered by a pension with a guaranteed payout has dropped from 60 percent to 10 percent in a little over thirty years.

Americans are going into debt faster than they're saving for retirement, and those able to put something aside often make wrong choices with their money.

Financial experts, who generally speak for the people with enough money to hire a financial expert, tell us to have $200,000 to $300,000 in personal retirement savings. Most Americans have about a tenth of that, less than $25,000.

5. Redistribution Has Moved Retirement Money from the Middle Class to the Rich

Tax Expenditures -- subsidies from special deductions, exemptions, exclusions, credits, capital gains, and loopholes that move tax money to the richest taxpayers -- are estimated to be worth up to 8% of the GDP, or about $1.2 trillion.

That alone is more than enough to pay for Social Security ($883 billion).

Because of this misdirected revenue, government has been forced to borrow from Social Security to fund its programs. Most notably, George W. Bush took our retirement money to pay for his two wars and his tax cuts for the rich.

This last reason, more than any of the others, reveals the overwhelming unfairness of cutting Social Security. In effect, the middle class is being told to replenish its own savings account after those savings were passed along to the military and the super-rich.

By PAUL BUCHHEIT